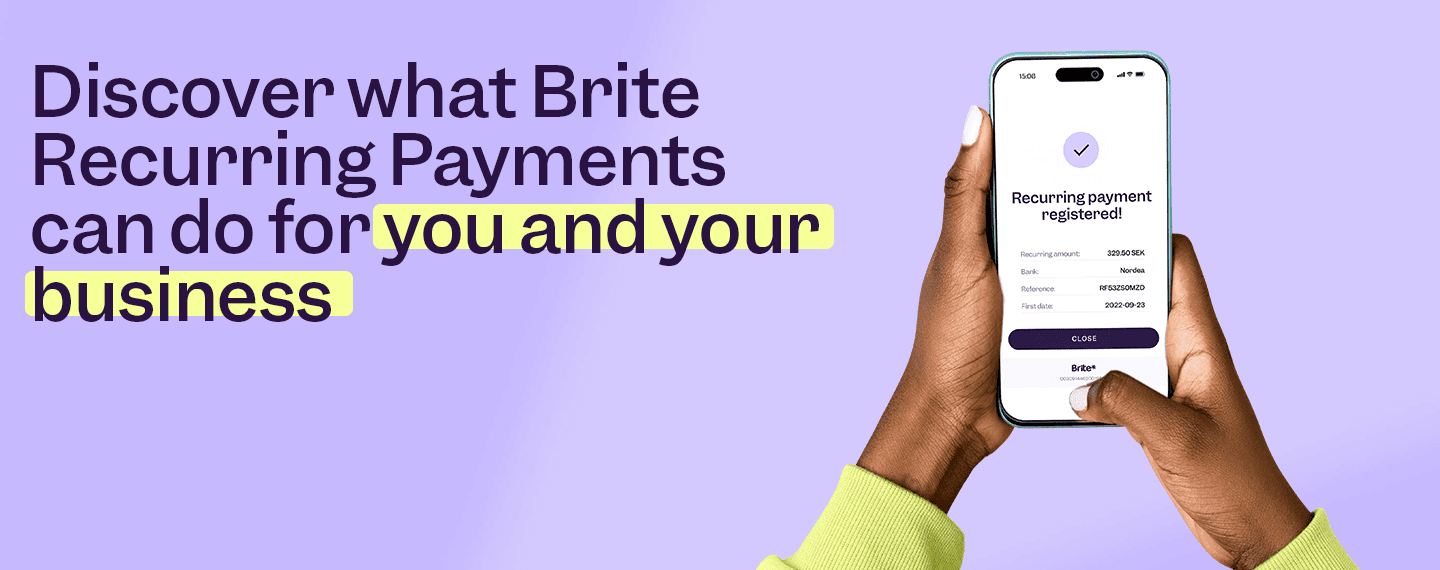

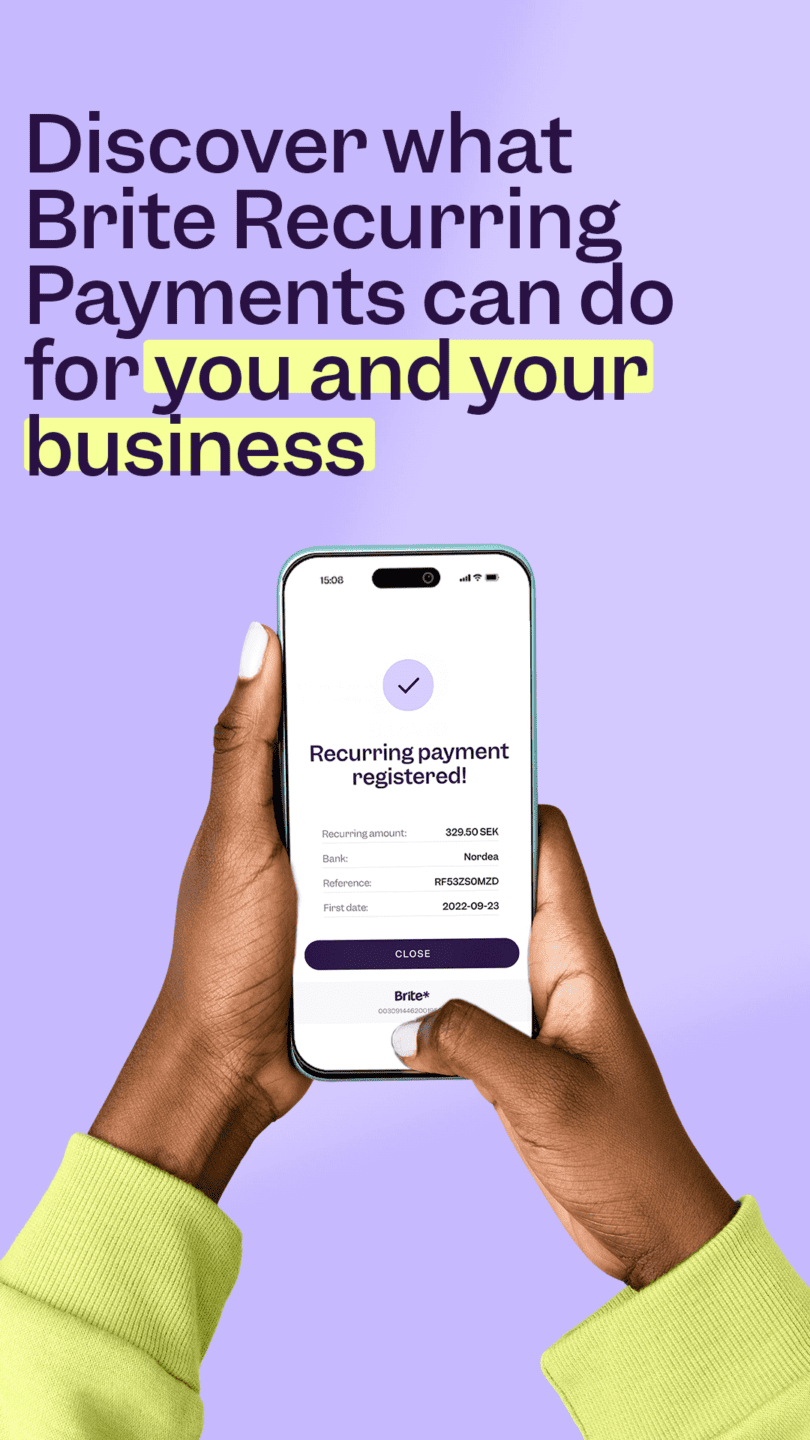

Traditional methods of processing recurring payments – usually a direct debit or credit card – are slow and prone to payment failures. Now, thanks to a new recurring payments service from Brite Payments, your company can harness the power of Open Banking to make recurring payments faster, easier and more secure.

With this new method, consumers no longer have to update their card details for subscription-based services every time their current card expires. So businesses using Open Banking to process recurring payments are able to benefit from a significant reduction in churn. And more stability in their cash flow.

Direct Debit vs Card vs Open Banking Recurring Payments

Direct Debit Payments

Since the first direct debits began operation as a paper-based system in 1964, it has remained a longstanding and popular way of processing recurring payments.

They are a familiar example of a ‘pull’ payment, where the payer gives the payee permission to regularly take money from their bank account. The payee initiates each payment, and decides how much to ‘pull’ and where it should go.

But despite its popularity, the direct debit process is slow – payments don’t happen in real-time – and open to misuse. Indeed, because of the potential danger of unscrupulous payees having complete control over how much money they take, the direct debit requires more guarantees and checks than any other method of recurrent transaction.

Card Payments

Cards are still the most popular way of making recurring payments, but they are also the most prone to churn. All cards have a limited lifespan and eventually expire, and many payments fail because users haven’t updated their card details. Recurring card payments have a failure rate of about 5%.

To pay with a card, users need to remember a long string of numbers, store their card details in a browser or, insecurely, at a merchant, or carry the physical card with them. These restrictions make card payments inconvenient, and negatively affect conversion rates.

Open Banking Payments

Open Banking is rapidly transforming how recurring payments are made. These Open Banking-enabled recurrent transactions require no cards, apps, or sign-ups. Users just choose their bank account and pay.

The world is beginning to recognise that the traditional systems of cards and direct debits are far from future-proof. In fact, Sweden plans to overhaul its entire payment infrastructure by the end of 2024. Primarily because of this very reason. This is a significant shift, and goes to show how great the demand is for a modern, faster, more secure method of payment.

What Can Open Banking Recurring Payments Do for Your Company?

Real-time recurring payments are not only faster and more convenient for customers. They offer significant advantages to the merchants collecting the funds. Here’s how they can benefit your business.

- Reduced churn – Half of churn (48%) comes from preventable failed payments. No cards means no expiry dates and fewer payment failures.

- Stabilised cash flow – No card details are required from consumers, leading to fewer subscription cancellations and account inactivities. This builds confidence in measuring and predicting future cash flows.

- Improved user experience – Faster, simpler onboarding, with minimal input required from customers.

- Empowered consumers – A new ‘push’ model of payment (vs. the longstanding ‘pull’ model used by direct debit) gives consumers more control over when and how they pay.

An Open Banking-enabled recurring payments solution can be combined with Brite Payments’ Know Your Customer (KYC) product ‘Brite Data Solutions’, which can automatically collect customer details and use them to register an account directly with merchants.

In combining these products with the subscription payments model in mind, Brite Payments has created an automated onboarding process that requires minimal manual input from the customer, optimising the consumer experience and reducing manual input errors.

What Makes Open Banking Better for Business?

In 2020, failed payments alone are estimated to have cost the global economy $118.5 billion in fees, labour and lost business. No cards means Open Banking payments have fewer payment failures. And with no card processing cost, they’re cheaper per transaction for merchants.

There’s also less waiting around. Open Banking settlements are made daily, so you don’t need to wait three- to five-days for funds as with traditional payment methods.

Finally, Open Banking-enabled payments have a higher conversion rate. They include automated collection of customer details to quickly register an account. And are designed with modern digital and mobile consumers in mind. All this ensures that payments are less manual and complex, leading to a 40% higher payment success rate. And the easy sign-up process for Open Banking payments means a smoother payment process, with less dropout.

Open Banking Puts Consumers in Control

The whole idea behind Open Banking is that consumers should have ownership over their financial data, instead of the financial institutions that manage their accounts and assets.

Open Banking turns the traditional payment authorisation model used by direct debit on its head, so funds traditionally ‘pulled’ from accounts are ‘pushed’ by consumers. Putting payment authorisation in the hands of the bank account holder gives consumers far greater control.

Recurring Payments on Time, Every Time

For online businesses that get paid on a recurring basis, Brite Recurring Payments is a payment method that makes it easy to sign-up and reduces churn because it works without cards that can expire.

It’s the smartest way to set up a standing payment order without the need of any direct debit mandating registration. Since it doesn’t rely on cards that can expire, you can rest assured payments will go through.

If your business needs to take recurring payments… let’s talk