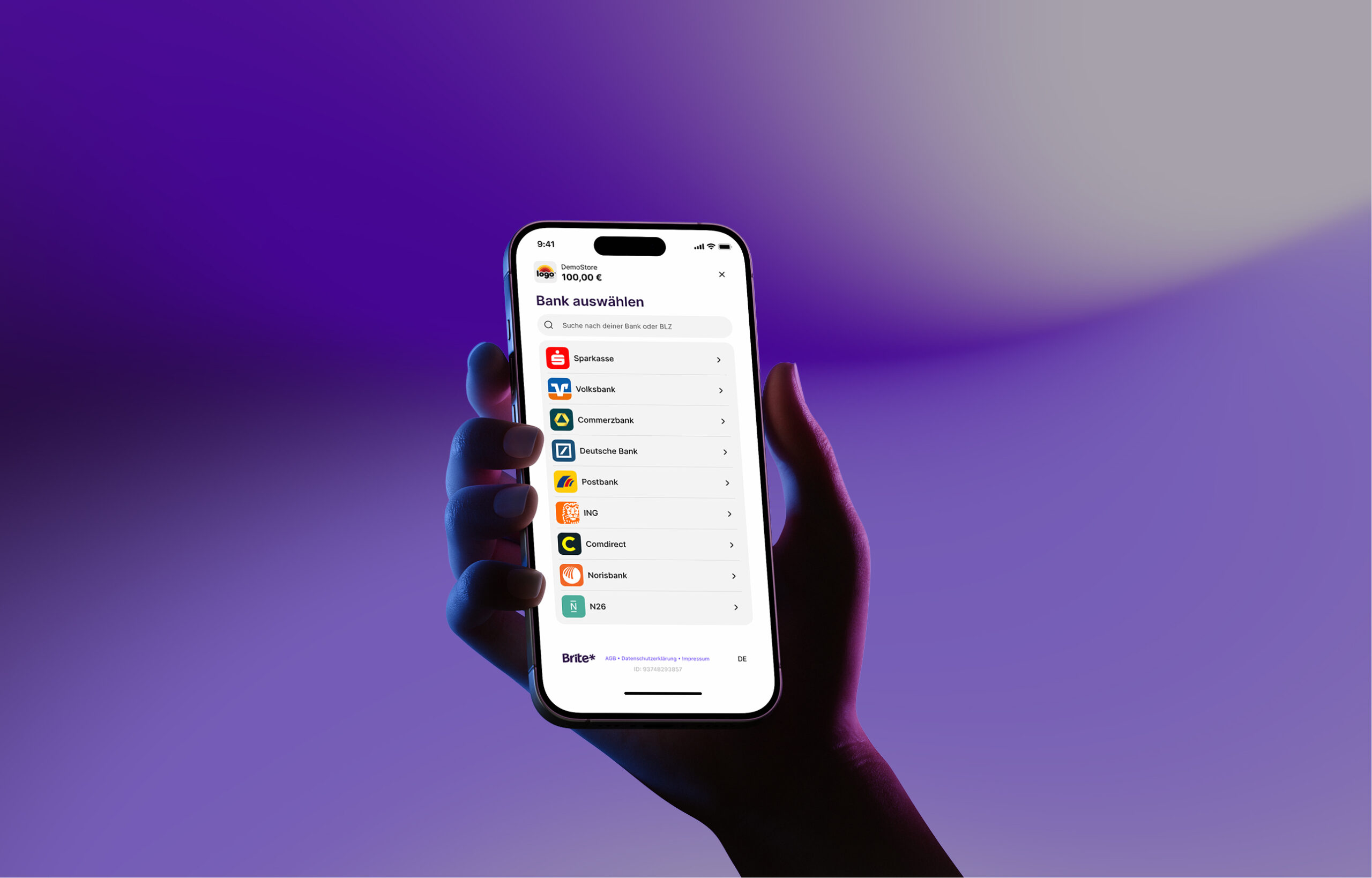

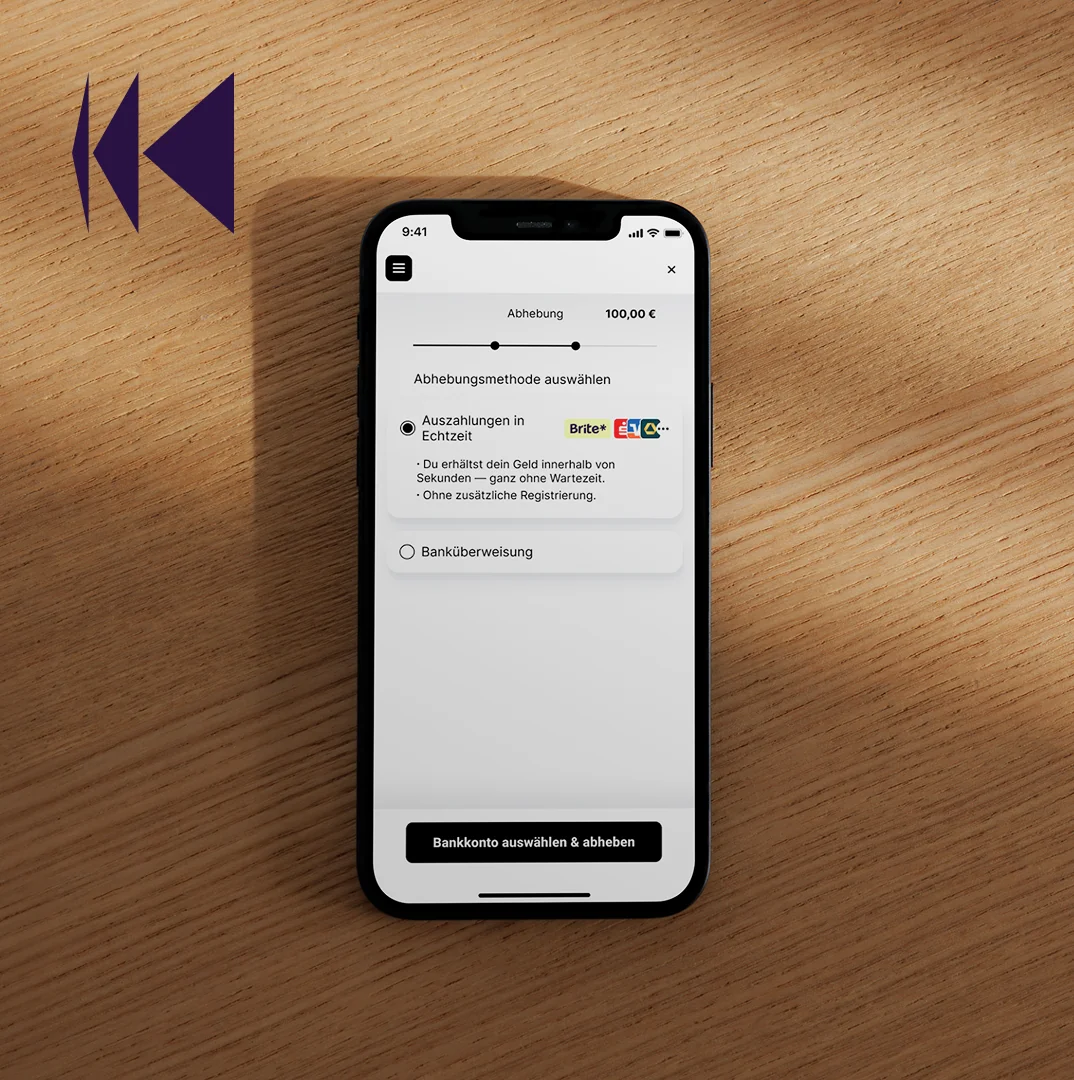

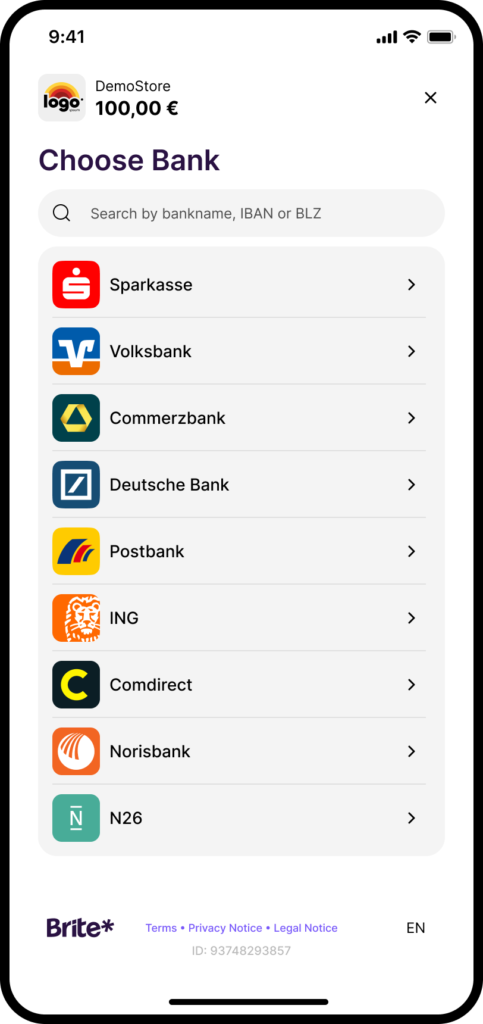

Unser Brite Instant Payment Network (IPN) ist an über 3.800 Banken angebunden und in 27 europäischen Märkten aktiv. Dies ermöglicht es Händlern, Einzahlungen, Auszahlungen und ihr Treasury europaweit zu zentralisieren.

Märkte, in denen Brite-Produkte verfügbar sind:

Belgien, Dänemark, Deutschland, Estland, Finnland, Frankreich, Griechenland, Großbritannien, Irland, Italien, Kroatien, Lettland, Litauen, Luxemburg, Malta, Niederlande, Norwegen, Österreich, Portugal, Rumänien, Schweden, Schweiz, Slowakei, Slowenien, Spanien, Ungarn, Zypern.