Throughout the rise of digital commerce, the most common types of payments have been bank transfers and card payments. Now, new forms of payments are emerging with mobile shoppers in mind: we call these instant payments, or account-to-account or even A2A. This article examines how the payments industry keeps up with evolving consumer demands by offering fast, secure payments and payouts.

Payments Types Available Today

Let’s look at incumbent payment methods. Starting with bank transfers and card payments, and why they longer cut it with today’s mobile-first customers.

Before Instant Payments Came Bank Transfers

The EU enjoys widespread bank penetration. Basic services like current accounts (checking account in the US) and savings accounts are widespread. Rather than dealing with cash daily, for safety and cost reasons, banks offer bank transfers (wire transfers in the US). These involve sending money from one private bank account to another. Instant payments can be seen as an evolution of the payments segment.

For businesses, the process is more complex. The traditional business-to-business payments model has six key players. There’s the business customer, the issuing bank, the settlement entity, the payments network, the acquiring bank, and the supplier of goods and services. Each pays transaction fees to facilitate the processing of non-cash payments.

For cross-border payments, it gets even more complicated. Technologies like the SWIFT network have handled overseas transactions since the 1970s. SWIFT is a messaging network using a standardised and encrypted system of codes (BIC, SWIFT ID, or ISO) to make overseas transactions for a variable fee. SWIFT guarantees the delivery of messages with a network and system availability greater than 99.999%. Still, it can take days to make and receive payments. This puts businesses and their customers in awkward positions concerning cash flow and repurchasing options.

Cards Were the Last Step Before Instant Payments

First introduced in 1958, by the 1970s cards were quickly becoming entrenched in most mature markets. Fast forward to 2022, there are nearly 30 billion payments cards in circulation worldwide.

The ubiquitous 8×5 cm PVC cards offer merchants the means to accept payments from all over the world but they present a less secure payment option than bank transfers. Card numbers can be stolen and used without the card owner’s knowledge. Moreover, merchants must pay a credit card processing company to accept card payments, eating into their profits. Issuers also target consumers. There are today up to eight standard credit card fees, including annual fees and late payment fees.

Costs aside, payments by card are more problematic than newer forms of payment, like instant payments, as they are subject to expiry every three to five years. This requires consumers to update subscriptions and payment details with potentially dozens of suppliers of utilities, entertainment, and other services. They are also prone to manual error if card information is entered into a payment system incorrectly.

These issues with card payments have inspired a new generation of mobile-first, agile and disruptive financial service providers. The new providers constantly innovate and adapt, offering new solutions and services to overcome such challenges.

Instant Payments and Instant Payouts

Historically, it was easy to understand the role payments companies have played in the ecosystem. But the landscape has begun to shift due to changing consumer expectations. Mobile-first payments, technological advances in device capabilities, and digitisation as the new normal. As such, new payment options are emerging.

In recent years, consumers have started to gravitate toward digital payment methods. Non-cash payments rose at a CAGR of 13% between 2018 and 2021. The COVID-19 pandemic further accelerated changes in spending habits, making this a lasting spending habit for many.

Real-time payments, also known as instant payments or account-to-account payments, present numerous benefits for merchants and consumers. They open bilateral communication and make transactions between businesses and consumers faster and more efficient.

Another advantage of instant payment flows is making payouts as quickly and seamlessly as possible.

Enabling finance customers like traders to enjoy friction-free payments with instant withdrawals means faster, safer re-investments and happier customers. Insurance companies can pay out in seconds for policyholders relying on insurance funds for repairs. Super-fast refunds from retailers will keep customers returning, while fast payouts for gig economy workers make them feel appreciated.

Payments generate considerable interest in the fintech space. The segment lead in total funding and deals in the fourth quarter of 2022. “About $3.4 billion was raised across 188 deals in the payments space in Q4 2022,” writes Mary Ann Azevedo in TechCrunch. “…nearly double the $1.8 billion raised across 62 deals by banking startups in the same three-month period.”

The Future of Payments is Brite

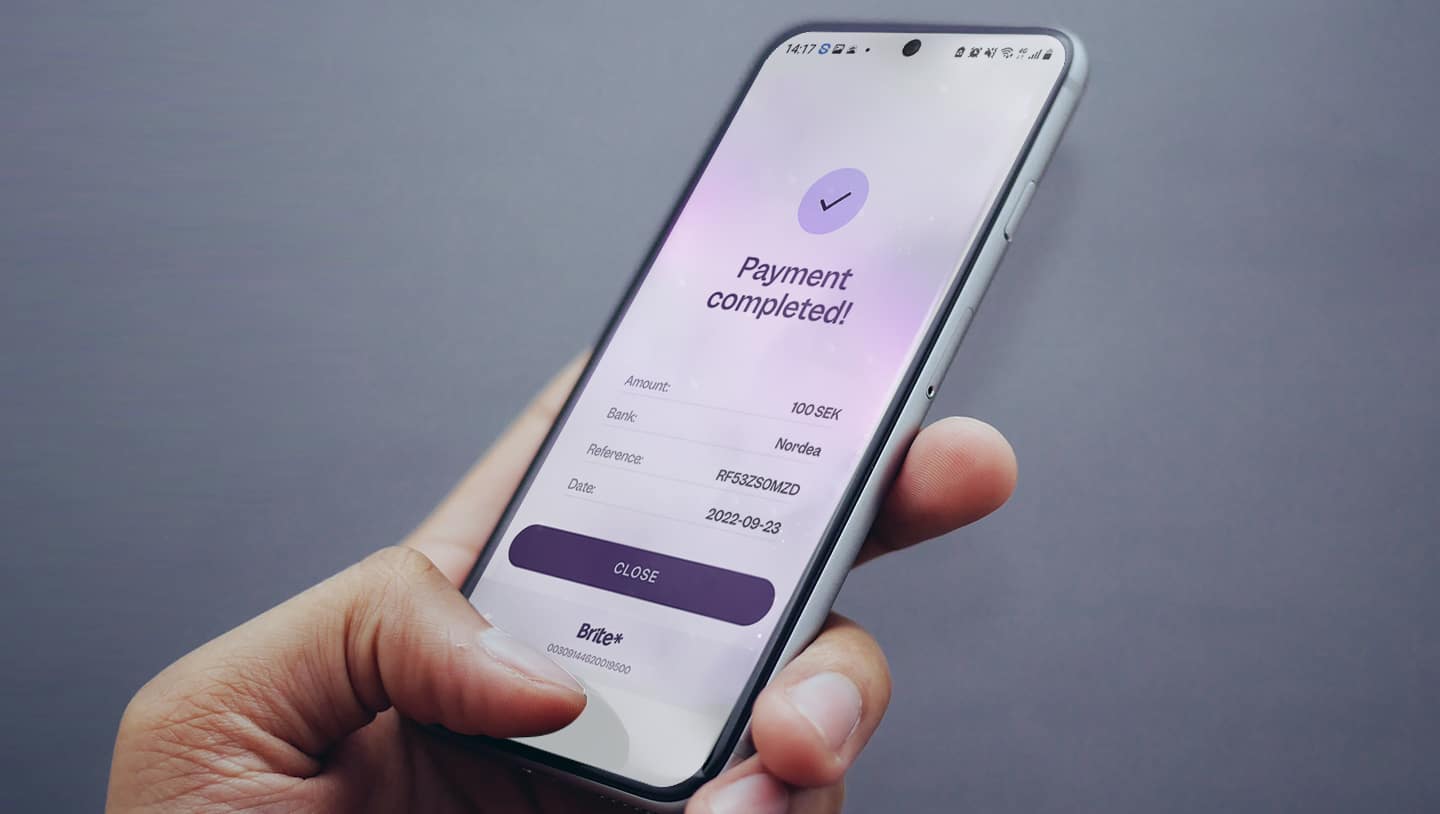

Today, in 2023, Brite Instant Payments offer a simple alternative to high-cost and slow payment methods and reliance on complex infrastructures. Brite Instant Payment services facilitate all forms of payment across Europe.

We recently extended our services’ coverage fully across the Baltic region. Our solution helps users pay up to 40% faster than standard instant payment flows. This provides greater convenience for consumers and better cash flow for businesses.

With Brite Instant Payouts, merchants can use open banking to securely and instantly. They can receive money from their customers, remove risk, improve cash flow, and reduce commission fees.

If you’d like to learn more about Instant Payments and Instant Payouts… let’s talk.