Scaleup Valley Podcast: Interview with Lena Hackelöer

The Ultimate Guide to Real-time Payments

This is the ultimate guide to real-time payments. Payment technology has evolved conisderbly over the past decades. Over the last century, cash, card and checks have been the go-to methods for businesses and customers alike. Meanwhile, B2B transactions, especially international and cross-border payments, have often relied on slow and expensive wire transfers. More recently, the introduction of electronic bank transfers has allowed us to make payments directly from one bank account to another. However, even today, the speed of electronic transfers remains dependent on a country’s banking infrastructure. This is causing unpredictable waiting times and significant uncertainty for both businesses and consumers. Following the launch of faster payments in 2008 in the UK, ‘instant’ or ‘real-time’ payment technology has increased in popularity. The global real-time payments market size is expected to expand at a compound annual growth rate (CAGR) of 34.9% from 2022 to 2030. It’s easy to see why real-time payments are becoming more popular in the ever-evolving digital economy. In this article, we’ll take a deeper look at real-time payments and their benefits for you and your customers. What are Real-time or Instant Payments? Real-time payments are monetary transactions made between bank accounts that are initiated, cleared and settled within seconds. This type of payment can be made at any time of the day or week, including weekends and public holidays. Real-time payments deliver a significantly faster, more consistent means of payment than most legacy payment rails. Legacy payment rails can take several days to reach a recipient. Instant payments are typically achieved by using a variety of technologies, and open banking can play a crucial role. Open banking-based instant payments allow consumers to pay by logging in to their bank with their digital ID. No need to download apps or use payment cards. The speed and security of real-time payments improve transparency and speed. This is helping banks, businesses, and consumers manage their money more accurately and efficiently. While enterprise (high value) real-time payments predominantly accommodate transactions between banks, ‘retail’ (low value) instant payments are perfect for small to medium-sized businesses and everyday consumers. What is SEPA Instant? Using the European payments infrastructure, the Single Euro Payments Area (SEPA) introduced an instant payments system: SEPA Instant Credit Transfer (SCT). SCT Inst is a payment-integration initiative led by the EU to simplify bank transfers (denominated in euros). The SEPA instant payment process includes sending a notification of the transfer to both the payer and the payee. The transaction is completed within 10 seconds. They are single, irrevocable payments capped at €100,000 and are only available in SEPA countries. This makes it possible for people doing business within supported countries to make cashless payments across borders with the same cost and convenience as domestic payments. However, participation in SCT Inst is not mandatory for financial institutions. So, while some European banks have been offering instant payments for some time, others have yet to communicate a date for when they will support the new system. Brite Instant Payments Explained Unlike SEPA, Brite Payments delivers consistency in instant payment processing across the Eurozone, regardless of its status with SCT Inst. Through its proprietary banking network, Brite utilises the optimised route for payment, using whichever rails are available. Using this method, Brite is not tied to the availability of SEPA. For online businesses who want to pay and be paid quickly, Brite is a payment method that offers fast transactions and reduced friction. Based on open banking technology. Users only need top-of-mind information, with no downloads or registrations required. Cutting-edge security measures keep customers’ money safe while being more cost-effective than any other payment method. The Benefits of Instant Payment Technology for Your Customers With funds more readily available and payments cleared within seconds, customers can be more agile in budgeting and cash management. Meanwhile, businesses can eliminate the time and resources typically associated with making payments, which boosts efficiency and aids growth. The 24/7 global nature of real-time payment transfers also allows for more flexibility and meets the rising expectations of merchants and consumers who value instantly available goods. Research shows just how much instant payment technology is valued across the world. A 2020 survey of consumers in six markets on three continents revealed that real-time payments are considered as important or more important than access to the internet, next-day delivery, and even everyday utilities. In addition, a staggering three-quarters of people said they would like all digital payments to be in real-time. Do Instant Payments Cost More for Businesses and Consumers to Use? In general, instant payments cost about the same as non-instant electronic payments, which is around USD $1.96 for 10 transactions per capita. A key benefit of the Brite Instant Payments is that users don’t need to pay fees. This is making it a more cost-effective option than other payment methods on the market. And by simplifying the payment process and cutting out the middlemen, businesses have access to more flexible, predictable pricing for better budgeting and financial visibility. The Next Generation of Payment Solutions By solving the payment challenges associated with paper cash and bank transfers, it’s clear that real-time payments are here to stay. Offering seamless and faster transactions, immediate access to funds, and a higher level of security, it’s time to cash in on instant payment technology. With Brite Instant Payouts, you can easily and securely use open banking technology to pay and receive money from your customers in one simple click. Gain peace of mind by removing risk, improving cash flow and reducing commission fees. If your business needs to transfer money quickly and safely… let’s talk.

Are We Moving Towards a Cashless World?

Cold, hard cash – it doesn’t hold the power it once did. As new digital payments emerge, is a truly cashless world on the horizon? Digital finance has accelerated rapidly since the start of the global pandemic; in the UK alone, 60% of the population will be open banking users by September 2023. But is it only the UK embracing the idea of a cashless economy, or is this trend seen worldwide? In this article, we will explore how different regions embrace digital payments and whether or not we are moving towards a cashless world. A Rapidly Evolving Payments Landscape The global payments market has undergone a huge transformation in recent years. Payment options as well as consumer expectations continue to evolve, and every region is adapting differently. A confluence of global events is reshaping the payments landscape. Everything from geopolitical factors and capital market resets to changing commerce expectations and societal responsibilities are coming into play. However, globally we see a growing payments sector and one with regional dynamics. According to McKinsey, globally, the number of non-cash transactions grew by 6% from 2019 to 2020. And in 2021, the overall volume of electronic payment transactions grew by 19%. These statistics clearly indicate that the global payments market is growing. But even in “less cash” economies where digital payments are widely used, “cashless” remains a more distant goal post. Will We Soon Be in a Cashless World? At this stage of maturity, digital payments are still a long way from being the sole, or even the primary, payment option in all regions of the world. But adoption is happening faster than you might think and in every corner of the globe. McKinsey found that within the EU, Greece and the Czech Republic had the sharpest reductions in cash usage between 2019 and 2021 – 15% and 12%, respectively. But it’s in many developing markets that digital payments are growing the fastest, across Asia, Africa, and Latin America. For example, Hong Kong, Colombia, and Peru all saw increases of roughly 50% in the volume of account-to-account (A2A) payment transitions in 2021. In Africa, Nigeria and some other countries saw their volume of A2A transactions growing in the 30–40% range. Adoption of digital payments isn’t only driven by consumers – merchants play a key role too. One study from Payments Europe revealed that 70% of European merchants would like to be allowed to refuse cash. However, this number varies greatly between countries, for example, 50% in Italy and 82% in Spain. This shows that cultural dynamics are impacting the adoption of technologies such as A2A and other digital payments. If Not Cashless, Maybe Cardless? While cash is clearly in decline in some markets, others hold onto it tightly. But does that mean digital payments don’t have a future in these markets? Not quite. Look at Germany as an example. It shows average or higher-than-average acceptance of cash compared to other EU countries. However, it also shows a higher-than-average level of acceptance of instant payments. In such regions, where cash has remained dominant throughout the credit and debit card era, we are beginning to see a different path to payment evolution. Instead of cash to cards, then A2A payments, markets like Germany may see more direct cash to A2A payment progression. Germany is just one (European) example of this possible pathway. For example, in many Latin American countries, cash has remained king due to many factors, such as a large informal economy, a lack of payment infrastructure for cards and high fees on card payments. Instant A2A payments present a significant opportunity in markets across Latin America. Unlike cards, which require a substantial infrastructure to support them, A2A payments only need internet access and a bank account. An estimated 76% of the global population have a bank account, and 83% have a smartphone. Combined with ever-improving internet infrastructure the barriers to adoption are decreasing. Local payment networks are also being established in regions such as Latin Americ to reduce dependency on international providers and support local businesses and policies. Local digital payment schemes, driven at the governmental level, have been wildly successful in some of the largest markets markets outside Europe and North America. For example, PIX, a payment method developed by the Central Bank of Brazil, and India’s Unified Payments Interface (UPI), are considered global leaders in consumer-oriented instant payments and are helping to bring greater financial inclusion to their diverse populations. The Next Generation of Payment Solutions We are not moving to a cashless world anytime soon. However, the digital payments market is in a period of rapid growth and evolution. It presents an opportunity for businesses to reposition themselves on the payments chessboard and win a long-term advantage. Businesses that adjust their payment models in a timely way to meet customers’ needs both globally and locally will benefit from the scale and flexibility that digital payments such as A2A offer. With Brite Instant Payments, you can use open banking to securely and instantly receive money from your customers in one click, removing risk, improving cash flow, and reducing commission fees. If your business needs to transfer money fast and safely… let’s talk.

Sweden’s Brite Payments Poised For Further Growth

Stockholm – 20 December, 2022 – Brite Payments, one of Sweden’s fastest growing fintechs, is in an extremely strong position to scale further as it enters 2023, on the back of tremendous growth over the past twelve months. The instant payments company has more than doubled revenue and transaction volume on its platform during a breakout year, as well as reaching a number of significant growth milestones. Over the year, the Stockholm-based second-generation fintech has expanded its operations to reach new markets in Europe, announced major commercial partnerships, launched several innovative new products, strengthened its leadership team, and received high commendation from industry peers. With its customer base growing, Brite has bolstered its internal operations, nearly doubling its headcount in 2022. The year has certainly been turbulent for the fintech industry, and while many companies have been forced to make cuts as a result of economic headwinds, Brite was able to advance its growth plans. The company made several high-profile additions to its senior team. This year saw the appointment of Lisa Edström, formerly Chief Compliance Officer at Zettle by PayPal, as its Compliance Director, as well as Jan Plasberg, formerly CTO of SOFORT and VP Engineering at Klarna to its board. Together, the new additions are helping Brite to build sensibly on a year of hypergrowth. In 2022, Brite helped to make instant bank payments even more efficient through the launch of its ‘Single Sign’ solution. The innovative one-step solution allows customers to pay straight from their bank account with only one authentication step, except for cases where regulation requires additional verification. Representing the next generation of instant bank payments, the solution has been shown to help users pay up to 40% faster than standard account-to-account (A2A) payment flows. Sofort collaboration Brite also announced its collaboration with popular online banking payment method SOFORT to launch a pan-European instant payout solution. As part of the agreement, SOFORT’s bank transfer product is now complemented by Brite Instant Payouts, and is available to SOFORT customers without any additional integration effort. This unique partnership is set to deliver greater speed and convenience to more than 80 million users of SOFORT in Europe’s largest markets, enabling them to finally take advantage of truly instant payouts. Reflecting on this year, Lena Hackelöer, CEO and Founder of Brite commented: “Demand for account-to-account payments has been gathering pace through 2022, which has helped to take Brite to new heights. We are strongly positioned in this nascent and rapidly expanding field, and helping an increasingly large base of merchants to deliver better user experiences, reduce customer churn, and improve acquisition rates with intuitive and innovative payment solutions.” “Brite has quickly become the payment provider of choice for businesses prioritising seamless and transparent solutions. As we continue to scale up our operations in 2023, our product coverage will expand beyond the 21 European markets that we serve today. Through more than 3,800 banks that are connected to our payment network, we offer simpler, safer, and more secure instant payments and payouts,” continues Hackelöer. International Expansion Thanks to Brite’s recent full launch across Estonia, Latvia and Lithuania, merchants in the Baltic region now benefit from the company’s full product coverage. The region, which has a population of more than six million, has long been at the forefront of digitisation and developing technical infrastructure. Brite’s now provides merchants and individuals with the ability to leverage the speed and efficiency of A2A payments and payouts for the first time. Brite’s tremendous work in 2022 hasn’t gone unnoticed in the wider fintech sector, with the company receiving recognition in several esteemed industry rankings. Most notably, Brite’s founder and CEO, Lena Hackelöer, has been named among the ‘Startup Elite’ in Tech Round’s ‘Top 100 Startups, Businesses, and Entrepreneurs in 2022’ list. Additionally, the payments innovator was revealed as the third fastest growing Swedish fintech by leading Swedish tech publication Breakit. As Brite moves into 2023, the company is primed for further industry recognition on the strength of its offerings. For more information about Brite, please visit: www.britepayments.com ABOUT BRITE Brite Payments is a second-generation fintech based in Stockholm. The instant payments provider leverages open banking technology to process account-to-account (A2A) payments in real-time between consumers and online merchants. With Brite, no signup or credit card details are required as consumers authenticate themselves with top-of-mind details using their bank’s usual identification method. The company currently operates across 21 markets in Europe and is connected to more than 3,800 banks within the EU.

Open Banking Benefits for Merchants – Brite interview

Open Banking has given merchants more choice and the ability to differentiate themselves from those using traditional payment methods. It facilitates the use of new and innovative payment methods that are faster, more secure, and provide a better customer experience. As a result, merchants who adopt these new payment methods can get ahead of the competition and create a more desirable consumer proposition. What are the biggest benefits for merchants when compared to existing payment methods? Open Banking has driven innovation in the payments landscape and opened up superior payment methods that meet the needs of today’s consumers. For instance, account-to-account (A2A) payments can offer significant benefits for merchants. Firstly, compared to card payments and the complicated pricing models connected to with this method, the cost of A2A payments is lower and more predictable. Furthermore, it is easy for businesses to integrate and create a better cash flow, which is a significant factor for consideration, particularly during periods of economic uncertainty. On top of that, A2A payments make the merchant proposition more interesting for consumers due to their security, speed, and ease of use. These factors are high on the list for consumer preference; therefore, they create better customer satisfaction and can help to increase brand loyalty. How has customer experience influenced payment innovation in the wake of Open Banking? The consumer desire for convenience has had a significant impact on payment innovation, asking for quick, secure, simple payment methods from merchants. There are a number of Open Banking-powered payment methods that illustrate this impact well. Consumers have made it clear that they require methods that make the payment process quick and easy. The Open Banking- benefits A2A payment method is crafted with consumer convenience in mind. All you need is a bank account, and users do not need to complete difficult sign-up forms or create more passwords. All they need is the top-of-mind information they would use to log in to their banking app, making the process very simple. Another consumer preference that we have seen influence payment innovation over the past few years is the desire to automate processes in order to make them easier. Consequently, we have seen the rise of Open Banking-powered recurring payments products entering the market to offer an automated/recurrent approach to subscription payments for example. The solutions allow monthly payments of a fixed amount to be sent directly from a customer’s account, without the need for updating or changing card details. This development is particularly valuable for people with long-term subscriptions who would currently face card expiry and hard detail re-entry every few years. Where do Open Banking-based payments stand to make the most difference in the near future? One of the most promising applications for Open Banking-based benefits in the near future is instant payments. With this technology, businesses and consumers can transfer money to each other in real time, without having to wait for the funds to clear through a bank. This could be particularly good for small companies, which often face days or even weeks for payments from their customers to clear. Therefore, instant payments stand to have a big impact on their cash flow management, which is timely given the current financial climate. In the retail setting, retailers are currently under pressure like never before to provide their customers with convenient and personalised payment experiences. Open Banking payments can enable a particularly easy user experience on mobile, for example, for in-app payments across multiple verticals. Therefore, this is likely to be another area where Open Banking-based payments stand to make the most difference in the shorter term, in sectors where we already see higher interest, such as retail, ecommerce, banking/finance, lending, marketplaces, media, entertainment, and telecoms.

How Gig Economy Payments Trends Point to a Sturdy Future

Flexible working models are nothing new, but they are growing in popularity. The number of global gig workers (non permanent employees providing specialist skills) will rise from 43 million in 2018 to 78 million in 2023. Gig workers are now vital to many businesses’ workforce and human capital expenditure. It offers businesses the flexibility to scale operations up and down based on demand. Besides, hiring gig workers is more cost-efficient when it comes to investing in human capital Gig workers also benefit from this new economy. They can have flexible work hours rather than bending to a traditional 9-5 work schedule. Given the important role gig workers play in our economy, it is curious that many still need to wait days, if not weeks, to be paid. Gig platforms that can guarantee fast or even instant payments for a job well-done stand to gain a massive competitive advantage. In this article, we will discuss the benefits of instant payments and why it is a must-have for businesses looking to hire in the gig economy. Gig Economy Trends: Instant Payouts According to Mastercard research, the forecast 78 million global gig workers will generate a gross volume of about $455bn by 2023. This is twice as big as in 2018. As the gig economy grows, it is becoming more regulated. Uber is a prime example. It received global backlash for how it treated its drivers because it referred to them as self-employed contractors. Due to a change in regulation, Uber has now had to recognise driver partners as employees. This then gives them some protection.The dynamics of gig economy workers are constantly shifting. Instant payouts allow businesses to build trust with workers where historically there was little. The Future of the Gig Economy Gig workers have become a vital part of businesses and valuable human resources. Many organisations now find that they have to start competing to attract the best workers. For gig workers, getting paid matters. Getting paid regularly, dependably, and without delay can greatly impact their lives. It can be the difference between only covering day-to-day expenses and planning for larger purchases – from professional development courses to a first home. Currently, many platforms make their workers wait days for payments. Why is there such a mismatch between the value that gig workers create and how they are treated? Not getting paid on time can damage the relationship between gig workers and their employers. They then start looking elsewhere for work. Fast and instant payments are the way businesses establish trust with their gig workers. Your business can build long-lasting relationships with temporary staff and set itself apart from the competition. The Current Payment Problem If instant payments are the way forward, why have they not been widely adopted? Currently, the gig economy relies heavily on bank transfers, batch payments, or business-to-freelancer invoicing (which can come with a service-level agreement (SLA) of 14-30 days. The bane of a freelancer’s life continues to be chasing invoices and in many cases paying a fee upwards of 3% to be paid within a week. But it doesn’t need to be this way. Freelance and gig platforms are quickly optimising the approval process between businesses contracting work and gig workers. For example, by streamlining the review and approval process. However, there is still a lot of room for improvement regarding paying out earnings once work is approved. The Next Generation of Payment Solutions Brite Instant Payouts enable independent gig-workers and businesses that employ them quick and secure payments from trusted sources across the globe. Rather than chasing for days, weeks, or even months for invoice processing or waiting for sporadic payments, workers can have money in their accounts instantly. Want to start offering instant payouts to your gig workers? Let’s talk.

The Ultimate Guide to Open Banking Security

Open banking offers consumers access to new and more competitive financial services. It is fast becoming a worldwide phenomenon. With approximately 12.2 million users in Europe in 2020, forecast to grow to 63.8 million by 2024. But building and maintaining a secure ecosystem will be vital to ensure this growth continues and the system has long-term success. EY research reveals that of those who have negative opinions about open banking, 48% cited data and cybersecurity concerns as their reasons for those negative opinions. Security will be a major factor in the future of open banking. In this article, we will discuss the rising concern of security in open banking and what businesses can do to ensure their funds are secure. Open Banking security: What is the problem? The challenge for open banking and payment service providers (PSPs) in Europe is to connect around 4,000 ASPSPs (Account Servicing Payment Service Providers) with the fast-growing number of potential open banking partners. APIs (Application Programming Interfaces) access underpins open banking. Essentially, APIs allow for fast sharing of data and ease of platform connectivity. This helps financial services connect with trusted partners who provide open banking solutions. However, APIs also present a big challenge from a security perspective. This is true in Europe, which is fragmented,with multiple standards and often bespoke APIs. There are currently no global consistent security standards to which Third Party Providers (TPPs) adhere, although there are some country specific standards that are broadly robust. Europe has mandated open banking through its payment services directive, also known as PSD2 which was established in September 2019. This framework formalised the relationship between European banks and FinTechs and mandated that European banks must give access to their banking infrastructure regulated TPPs via APIs. However, there is no universal standardised API in Europe, or in the UK, that these banks must meet. While the PSD2 regulation makes a good start on security, it does not specify details about the APIs. TPPs can create APIs how they wish, with only the technical framework conditions being specified. The clear issue stems from some APIs being developed with a higher priority on security than others. Bad actors will quickly find the weak link in some APIs, and when a sensitive data exchange takes place between clients of a bank and a TPP, there is a ripe opportunity for them to attack. How can Europe mitigate open banking security risks? Collaboration and standardisation PSD2 mandates that TPPs must identify themselves to ASPSPs to gain access to accounts and to connect with banks. The ASPSP then needs to authenticate the payment service user. When data is being exchanged during this process, personal and financially sensitive information must be kept secure and not be accessible by anyone other than the bank and the TPP. For this to happen, all parties involved must collaborate. Currently, all TPPs need to be licensed by a European financial services authority. However, banks across the globe are launching their own open Banking APIs without the need for TPPs, which will cause further security gaps due to multiple standards based on individual, organisational security protocols. To build a secure ecosystem for consumers, collaboration and standardisation need to be a priority for all involved. Not only between banks and their FinTech partners but also between regulators and government agencies. We may see greater standardisation coming in future as protection against payment fraud is high on the agenda for the PSD3 consultations. The revised directive will possibly look to ensure top-level consumer protection. However, PSD3 is still far off, and will probably come into practice in the next three to five years. There is much work to be done in the meantime. Transparency Another security area that TPPs and banks must improve is transparency. Transparency is paramount to building trust with consumers and creating high-level security protocols. In Europe, businesses are legally required to inform customers about what their data is being used for, how they can control it, storage procedures and how the business is audited and regulated. There is already a fair amount of regulation around data privacy and an established culture of transparency. The idea behind open banking is to give customers control over their data, which means they can opt out of these platforms whenever they choose. As such, TPPs and banks should feel encouraged to provide greater data protection for their customers. Customer education Another hurdle to overcome is consumer education. There needs to be collective education about the possibilities that pen banking provides and guidance for how to behave securely when sharing financial assets and personal data with TPPs. But there is the looming question of where the responsibility for this education lies. Is it up to governments and regulators to educate? Or should the responsibility fall on businesses and providers that are bringing open banking products to the market? Secure Open Banking with Brite Payments – the next generation of payment solutions Open banking may have some security concerns, but those bringing the products to market can work to minimise the risk. Much of the responsibility to improve open banking security in Europe will fall to regulators to create a standardised API security framework for banks and TPP to adhere to, which we may see come to light in the years ahead. Brite Instant Payouts is an open banking service that allows you to securely and instantly receive money from your customers in one click, removing risk, improving cash flow, and reducing commission fees. If your business needs to transfer money fast and safely… let’s talk.

How to Prevent Payment Fraud and Chargeback Fraud

Chargeback fraud, in its various guises, is predicted to reach $117 billion in 2023 – with merchants shouldering the vast majority ($79 billion) of this. Chargeback fraud is a major contributor to payment fraud, and the costs continue to rise. How much are unauthorised payments, merchant error, Card Not Present (CNP) fraud and friendly fraud costing your business? Here, we look at the scale and sources of payment fraud, how it can affect any business that processes card payments, and how secure instant payments can help prevent it. What is Payment Fraud? Payment fraud and chargeback fraud comes in a variety of forms. The methods of fraud contributing most to the startling business losses outlined above include: Chargebacks Chargebacks are one of the biggest financial costs faced by merchants. A LexisNexis study of ecommerce and retail businesses reveals a substantial increase in both the cost and volume of chargeback fraud. For every $1 of fraud, U.S. retail and ecommerce merchants now pay $3.75 – 19.8% up on pre-Covid levels. Introduced to protect customers, chargebacks happen when a customer disputes the legitimacy of a transaction charged to their account. Merchants can contest a chargeback claim, but the process can be slow and laborious. Because of this, many merchants choose to accept chargebacks, even if they believe a transaction was legitimate. Although chargebacks can take a variety of forms, the result is usually the same – the merchant pays to reverse the transaction. Counting the cost of chargebacks The question of ‘how much do chargebacks cost?’ is tricky to answer. Just as there are many factors that influence how many monthly chargebacks your business will face, there are also multiple factors that can impact their cost to you. Any time a business faces a chargeback, it will lose any revenue from that sale. But there are also a number of ‘hidden’ costs associated with chargebacks you might not be aware of. These include: All in all, the average cost per chargeback is $191, based on a $90 average disputed transaction. As a rule of thumb, the total cost of each chargeback is usually between two and three times more than the initial transaction itself. With global chargeback volume reaching 615 million transactions in 2021, according to Mastercard, we can begin to understand the scale of the costs to businesses. And can well believe the projected total cost of chargebacks in 2023 of $117 billion. The Rise in Friendly Fraud Dismissed by some as a mere cost of doing business, friendly fraud can take two forms: Typically friendly fraud is used as a broad term to describe when a customer files a chargeback on a legitimate transaction instead of first approaching the merchant for a refund. Chargeback losses for businesses are rising. An estimated 10.4% increase between 2021 and 2023, in fact. A large factor in this increase is the rise in ‘friendly fraud,’ which is expected to account for around 60% of all chargebacks filed in 2023. Friendly fraud is very hard to mitigate, and particularly prevalent in digital goods. Instant account-to-account (A2A) payments are one way to tackle this problem. Prevent Payment Fraud and Chargebacks with Instant Payments Traditional payment method providers are working to combat payment fraud. Credit cards are subject to increased authentication measures across industries, for instance. But shifting to an open banking-enabled secure payment service, like Brite Instant Payments, reduces the risk of chargeback- and friendly fraud to near zero. How Brite Instant Payments Prevent Payment Fraud and Chargeback Fraud Instant Payments from Brite give you more conversions, more returning customers, and more revenue. With less fraud, chargebacks, and middlemen. With chargebacks and payment fraud on the rise, merchants need to find a solution and stem these losses as soon as possible. By shifting payment flow from card payments to open banking-enabled A2A payments, merchants can significantly reduce their exposure to the risks of chargebacks and payment fraud. Avoid the Cost of Chargebacks and Payment Fraud with Brite Payments Brite Instant Payments drastically reduces the chances of fraud. By transferring money to merchants instantly, Brite simplifies the payment process by cutting out the middlemen. With instant A2A payments, merchants have more control over chargebacks – and the rising cost of payment fraud.If your business needs to cut the cost of chargebacks and payment fraud… let’s talk.

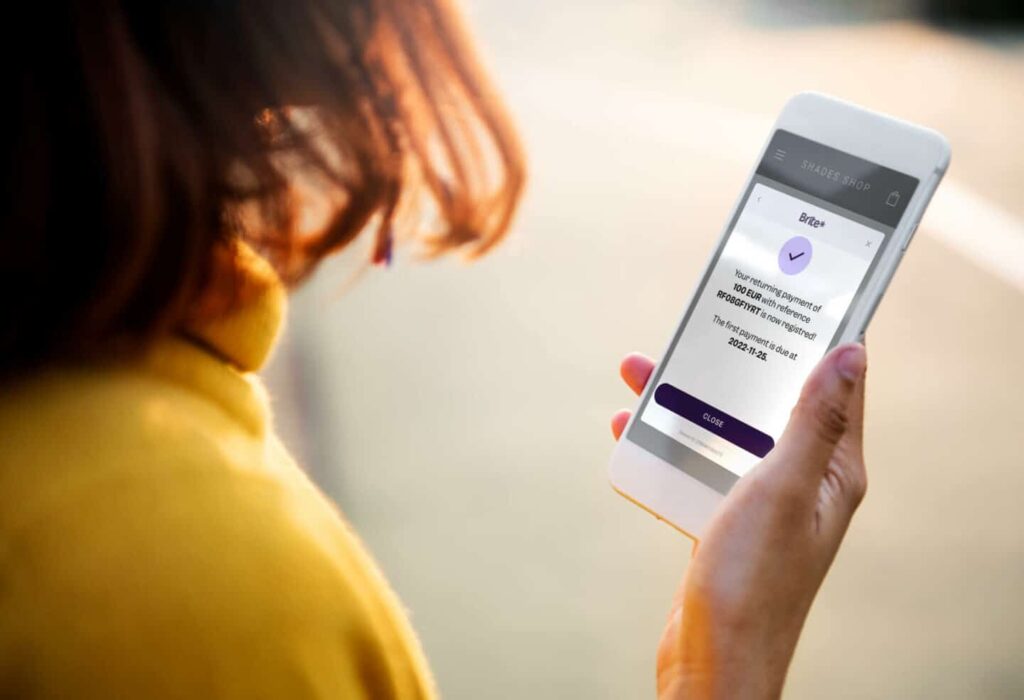

Solve Involuntary Churn With Secure Subscription Payments

Subscription payments account for 5% of all consumer spending in Europe. At first glance, this might seem like a small number, but in reality, it’s a sizable chunk. Subscription services are often paid for with recurring card payments. But credit and debit cards normally have a life cycle of only three to four years. As a result, involuntary churn – either through expired cards or out-of-date information – is responsible for almost half (48%) of all total churn. Involuntary churn is an avoidable problem for companies. Secure recurring payments directly from your customer’s bank accounts remove the possibility of expired card information that causes involuntary churn. This article examines how cardless recurring payments can help businesses with subscription models tackle involuntary churn. The Pitfalls of Cards for a Subscription Model Credit and debit cards weren’t designed for recurring payments. They are part of a complex infrastructure that goes through multiple players, often looking something like this: This kind of infrastructure does not well support recurring subscription payments. It’s too complex and every time a payment is taken has to go through the same system. Another major reason that card infrastructure does not support subscription models is that card details become outdated over time as they expire or are lost or stolen. They can also fail because customers reach their card limit. To avoid these pitfalls in the card ecosystem, A2A (Account to Account) recurring payments are a new alternative. The Benefits of Cardless Payments for your Subscription Business Brite Payments’ recurring payments service lets businesses set up a standing payment order without any direct debit mandating registration. Essentially what this means is that your customers can send their subscription payment directly from their bank account. As this payment method doesn’t rely on cards that can expire, you know that your payments will go through every time. Reduce Churn Subscriptions will not be terminated or become inactive due to a lack of payment details. Card churn is significantly reduced, which lets your business improve the stability of its cash flow. Improve Cash Flow Recurring payments that are set up without cards allow you to be better able to predict cash flow, in turn influencing your business strategy. Reduced churn helps you get more value from your customers and have a higher chance of payments being collected. You are not caught off guard one month by a spike in failed payments. Save Resources Additionally, fewer resources are spent providing email or telephone support. Both from automated emails and customer service calls. The same applies to debt collection. With recurring payments, your team no longer spends time chasing after missed payments, freeing up their time to focus on other areas, such as business growth. Lower Administrative Costs Administration fees are also significantly reduced with subscription services, removing the need for Strong Customer Authentication (SCA) in every transaction (it is only required for the initial payment setup). Overall, recurring payments create greater operational efficiency while also improving your service. The Benefits for Your Customers Not only does your business benefit and a massive headache get removed from your sales team, but your customers will thank you too. Recurring payments completely eliminate your customers’ need to update their account information. Improved Customer Experience Have you ever lost your wallet? Not only were you frustrated at the loss of your ID and cash, but you had to cancel your credit and debit cards. You likely then got numerous emails and calls over the coming months reminding you to update your card information for services like Spotify, Google Drive, Netflix, or Adobe Creative Cloud. Services often freeze until you update your details. This can be a headache and time-consuming to remedy. You can remove this problem for your customer by setting up A2A recurring payments. Tackling the Root Cause of Involuntary Churn Rooting out the major cause of involuntary churn means reducing your business’s reliance on cards. By using A2A payment methods, you can dramatically reduce failure rates for your subscription charges. Businesses that use subscription models have been keenly aware of the issue of involuntary churn for years. As such, numerous solutions to the problem have cropped up but without delivering significant results as they don’t tackle the root of the problem. For example, Stripe Billing claims to help decline failed payments for subscription services. It claims to reduce payment failures by 38% – if you start with a 10% failure rate, you’ll reduce it to 7.2%. This method uses account updaters but is limited as your customers need to be signed up for it to function. Instead, getting to the root of card declines – cards – could reduce your failure rate even more, cutting involuntary churn significantly and ultimately enabling you to increase every customer’s lifetime value. Brite Payments: Built for the Subscription Economy With Brite Payments, you can securely collect recurring subscription payments directly from bank accounts. There’s no manual entry, no expired cards, and no involuntary churn.If your business needs to collect subscription payments and reduce churn… let’s talk.

3 Ways to a Leaner, More Modern Payment Infrastructure With Open Banking

A2A (Account-to-Account) payments currently account for 13% of all checkouts in Europe, and that number has steadily increased over the past few years. In Europe, 20 countries are part of the centralised instant SEPA credit transfer (SCT Inst) scheme used for A2A payments and simplifying bank transfers in Euros. A2A payments are a growing trend and, in the coming years, will become the ‘new normal’. In this article, we will explore what is driving that trend and why A2A is the ideal replacement for card transactions. What are Instant Payments? A2A payments fall into two categories: Although A2A payments have been around for a while, they are only now starting to become part of the mainstream and initiatives such as SEPA are helping drive that change. What is SEPA? SEPA stands for the Single Euro Payments Area and is an instant bank transfer scheme introduced in 2017 at the request of the EU. The purpose of the scheme is to enable easy and instant cross-border payments across the EU, with 20 countries already signed up. SEPA presents new opportunities for merchants and customers. From penetrating markets with low credit card use such as Germany and the Netherlands, where credit card use is lower than 50%, to improved cash flow from merchants by being able to collect payments when they want. However, the current state of the market has some downsides. Firstly, adoption has been slow, so there are regions where it is not being used. For example, in the Netherlands, where adoption is high, there were 3.312 billion SEPA transactions in 2021. In contrast, in Denmark during the same year there were only 4.3 million. Another issue that merchants need to consider is that SEPA uses two different infrastructure solutions, RT1 and TIPS (run by the ECB). Banks can choose to opt into either, but they aren’t interoperable. This means that a bank using TIPS can’t make an instant payment to a RT1 participant and vice versa. Integrating both means greater cost and effort on the banks behalf so there is not the motivation to do so. Brite Payments as a SEPA Solution Brite Payments solves many of the current issues that merchants face with implementing SEPA payments. They are building connections and integrations across Europe, and already covers 3800 banks, including ING, Citadele, SEB and more. This translates into a payment solution that is easy to embed at checkouts for both payins (in the Nordics and Baltics) and payouts (in the Eurozone). Merchants don’t have to choose between RT1 or TIPS, they can use a solution that integrates with banks on both sides. Hence, with the current growing pains that SEPA is experiencing, Open Banking payments are the ideal replacement for cards and we will see greater adoption in the near future. Why are Open Banking Payments an Ideal Replacement for Cards? There has been a long-standing card dominance within the payment landscape, but that reign is coming to an end. Merchants and customers are seeing the benefits of Open Banking transactions and the demand for them is growing. One of the major benefits for merchants is that A2A payments eliminate chargeback risks and costs. Midigators Year in Chargebacks report shows that 2.31% of merchants revenue was lost to chargebacks in 2021. This can have a huge impact on your business and its bottom line. A2A payments present the opportunity to move to a leaner and more modern payment infrastructure that avoids this kind of problem. Here’s three ways how: 1. Lower Transaction Costs Firstly, A2A payments via Open Banking can have significantly lower per-transaction costs than card payments. Your business may be making hundreds, if not thousands of transactions a day and these savings quickly accumulate. Typically a card transaction fee is around 3% but by using A2A payments, your business bypasses this infrastructure and in turn, its cost. 2. Less Friction for Customers The second way businesses can improve payments with A2A open banking is by providing a better experience for their customers. How many of your customers abandon carts at checkout because of a poor payment experience? With A2A, instead of your customer’s credit card provider mediating the payment, there is a direct transfer from their bank account, making a frictionless experience for your customers (and for your business). 3. International Reach Thirdly, A2A allows your business to expand its reach and attract customers in new locations. Your business can reach anyone with a bank account, which, let’s face it, is the majority of the global population (71%, to be exact). The Next Generation of Payment Solutions A2A banking is becoming mainstream and the time for merchants to get on board is now. It frees you from the restraints of card payments and presents numerous new opportunities to grow your business. If your business needs to pay out money fast, or if you want to make paying for your customers seamless… let’s talk.