Payment technologies and new payment methods are helping to shape consumer payments within the instant economy.

Indeed, the instant economy is constantly evolving, meaning growth opportunities are up for grabs for fast-acting and forward-thinking businesses. How? By giving customers the same level of convenience, speed and security in their payments as they’ve come to expect elsewhere online.

To learn more, we’re exploring insights from our latest report on the instant economy. In early January 2024, we surveyed six key European markets together with YouGov on customer attitudes towards online payments and different technologies, amassing nearly 8,500 respondents. Read on to see how you can capitalise on the latest trends in instant payment processing and prepare your business for the future.

The rise of instant payment technologies (in brief)

Though its journey started in Japan in 1973, instant payment technology is finally seeing mass global adoption, with most countries having launched instant payment processing systems within the last 10 years.

This wave of new technologies that deliver speed and security (not to mention some government carrot-and-stick measures to grease the wheel) means that customers can now make real-time transfers in over 97 countries.

While card usage lingers in most regions, India and the EU are particularly strong markets for payment innovation, with the Netherlands a highlight, according to our Instant Economy report. What’s more, the next five years will be especially promising in adopting new payment technology, according to industry commentators.

The two key types of instant payment technology across Europe

Account-to-account (A2A) instant payments

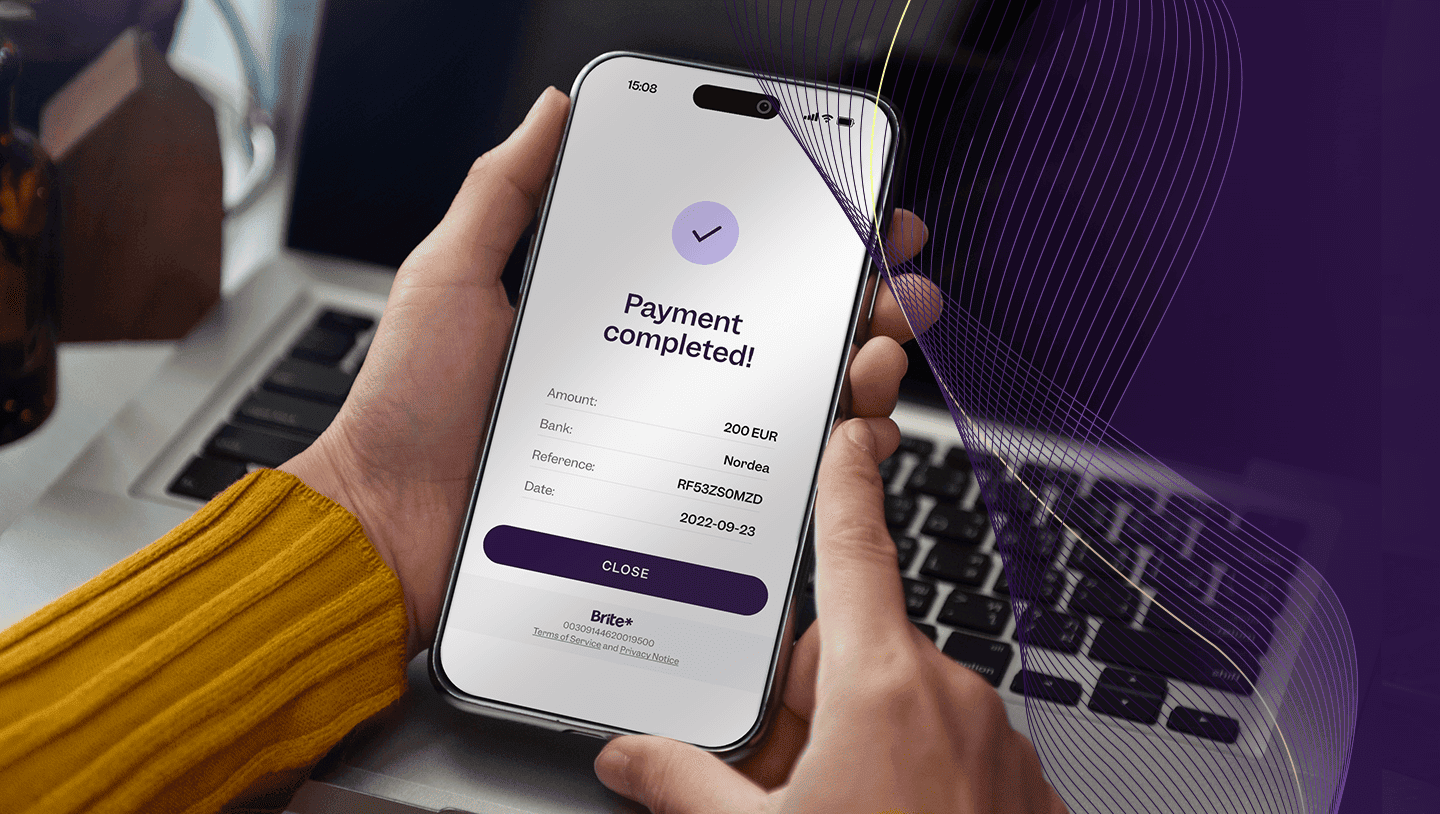

Open banking powered account-to-account (A2A) instant payments are the leading force behind Europe’s instant payment processing systems – often called “Pay by Bank” when in checkouts or consumer-facing conversion points. You can read more about the benefits of this type of payment method in our in-depth A2A payments explainer.

The interconnected banking infrastructure means customers can quickly and easily send payments via Single Euro Payments Area Instant Credit Transfers (SEPA ICT) in 10 seconds or less, usually within a person’s native banking app.

However, proprietary networks like Brite IPN also exist to bridge regional gaps in instant payments processing coverage and give businesses seamless access to the instant economy.

Digital wallets

Digital wallets are another type of instant payment technology available to customers. Most commonly used digital wallets are ‘open’ or ‘open-ended’, meaning they can interact with any merchant that supports the technology (online, in-store, etc.).

This is because digital wallets are mostly provided by banks or financial institutions that build proprietary integrations across different payment ecosystems – namely, card networks, bank transfers, on-platform accounts, and so on – to improve the user payment experience. Examples of digital wallets include those provided by Apple, Google and Samsung.

Generational preferences for digital wallets and Pay by Bank

Our survey Instant Economy Payment Insights report found that paying preferences aren’t consistent across all age groups, as instant payment technologies are more popular with younger consumers . For example, Generation Z’s (18-29 year-old in the Brite report) favourite payment methods are debit cards, digital wallets, and Pay by Bank – with the latter two virtually interchangeable. This popularity is largely due to the lack of additional fees as well as the speed and security of instant payment technologies.

By contrast, older consumers (those aged 50+) tend to opt for traditional payment options, like credit and debit cards, since they’re familiar methods and can also help improve their cash flow at the same time. However, the adoption of instant payment technologies as a whole was strong, as every generation across Europe was either an existing regular user or someone willing to try them.

Examples of digital wallets and Pay by Bank methods across Europe

Cross-border instant payment technologies like SEPA ICTs and Brite’s IPN or digital wallet providers like Apple and Google offer international instant payment processing solutions.

However, across the Europe there are many local or different methods of digital wallets and Pay by Bank – here is just a taster of what is available. Regional digital wallets and instant payment processing providers include:

1. iDEAL

iDEAL is a Dutch online instant payment processing system that allows customers to use their bank account rather than a credit card. Launched in 2005, iDEAL handles more than 1 billion transactions annually and is supported by integrations from over a dozen Dutch financial institutions. Users can pay for online goods and services, including household bills, subscriptions and even other users via third-party integrations.

2. Bizum

Bizum is another Pay by Bank digital wallet provider based in Spain and one of the largest regional brands on our list. Founded in 2016, the platform has quickly amassed a network of 38 affiliated banks, offering seamless instant payment processing to nearly 60,000 online merchants to its 25+ million users. Bizum allows users to send and receive funds to both businesses and peers in less than 10 seconds and has handled over €138 billion in total value since its inception.

3. Mobile Pay

Mobile Pay is the leading instant payment processing provider across Finland and Denmark. This Nordic financial services powerhouse boasts over 6 million users, 50+ partner banks and €23 billion in 2021 revenue alone. Much like the previous entries on our list, Mobile Pay enables instant payment processing for both business and peer-to-peer accounts.

4. PayPal

PayPal is one of the most well-known financial services brands on our list. In addition to its strong international adoption, PayPal receives around 130 and 70 million monthly visits from Germany and the UK, respectively making it particularly important in those markets.

Founded in the late 90s, the company has heavily diversified over time. It now offers various payment services, including instant processing for traditional and novel payment methods, like cryptocurrency, via its extensive digital wallet. What’s more, PayPal hosts a number of sub-brands enabling instant payment processing via Venmo, Xoom and many other services for businesses and end consumers.

5. Sofort (now known as Pay Now)

Finally, Sofort (now known as Pay Now) is a German instant payment processing provider that’s particularly popular in Germany, Finland, and the Netherlands. Now in the middle of rebranding under its parent company, Klarna, Sofort enables instant online and in-store payment processing and has grown its user base since its 2005 founding to over 150 million customers.

Stay ahead of instant payment technologies with our latest report

Business leaders must constantly modernise the payment technologies they offer at checkout for seamless transactions and reliable revenue streams. To learn more about the current and future state of online payments across the instant economy, download and read our latest report.

In it, we go in-depth on customer attitudes and perceptions of the latest payment technologies, payment preferences, and share never-before-seen insights from six key European markets. Get your free copy today to find out more and ready your business for the future: